Article

The Changing Moods of the Stock Market: Reading Market Sentiment

It is no secret that the stock market is primarily driven by two sentiments: the fear of evil and hope for good. Within these broad emotions, we encounter speculation on rising share prices and the anticipation of future earnings. Conversely, we also find the fear of falling stock prices, economic crises, recessions, and collapses.

I devoted part of my university studies to understanding moods, what they are and how they change. Therefore, it is not surprising that this topic also interests me in the context of the stock market.

How I read market sentiment: my mood thermometer

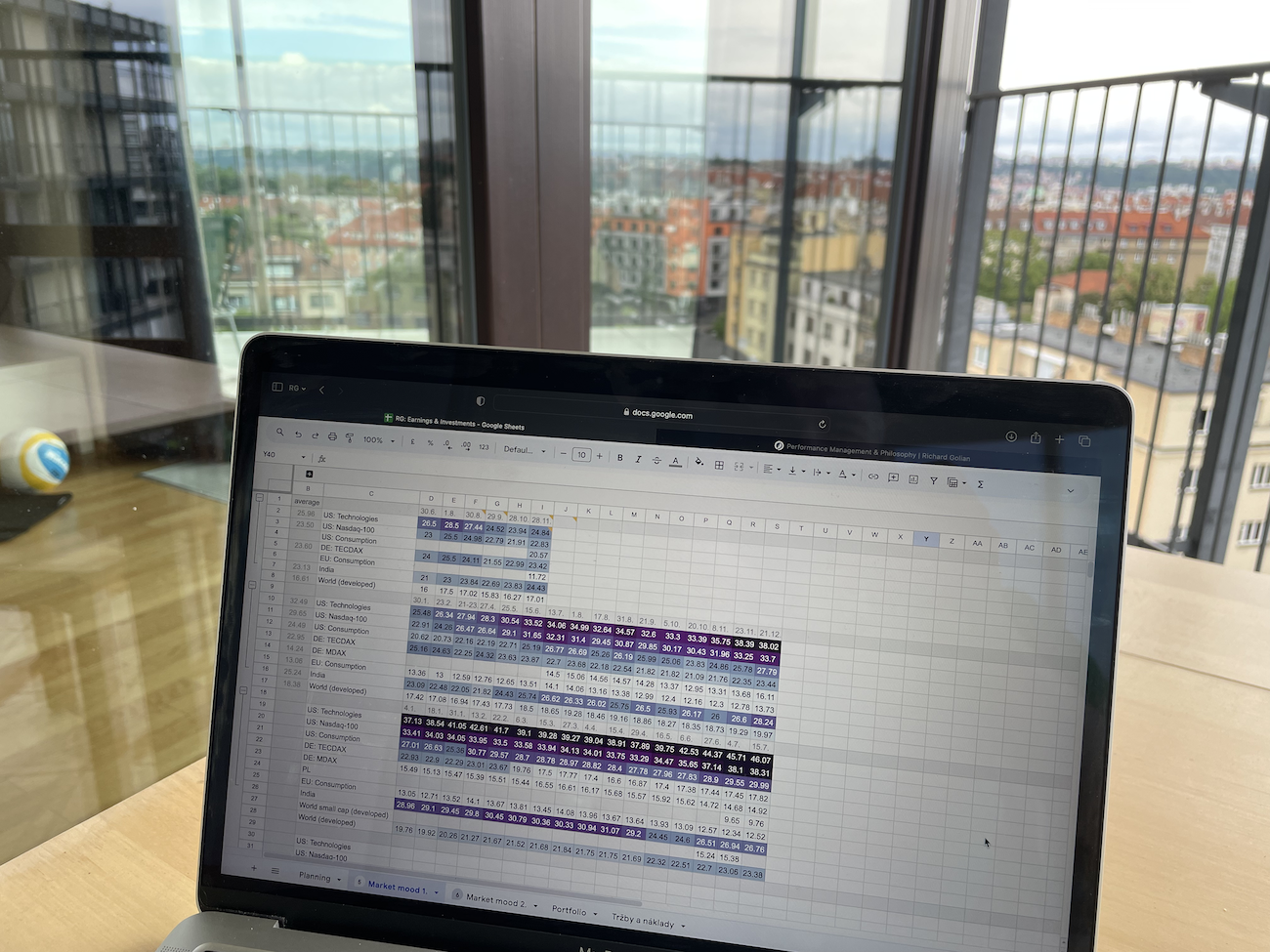

A mood directed towards the future, such as hope for growth or fear of downturns, can be observed through various data. I find it logical to track asset prices within specific segments (geographical or sectoral) in relation to how these segments generate earnings and their value. I compare this data with historical data within the same segment, data from other segments, and the entire stock market's performance.

I use data published by various indexes and ETF funds. As you might gather, I am not analysing individual shares but collections of shares grouped by specific criteria (read more about stock indexes and ETFs). Since 2022, I have been tracking this data, documenting what the media says about the economy and the stock market, and noting factors that could influence sentiments. This forms my “mood thermometer.”

Join the Library

Full access to my thoughts, personal stories, findings, and what I learn from the people I meet.

Join the Library · €29.99 per yearGet the full article by email and feel free to reply if you want to discuss it further.

Disclaimer

This article is intended for informational and educational purposes only. It does not constitute financial advice, a recommendation to buy or sell any securities, or a guarantee of future market performance. The views expressed are solely those of the author, who may also be an investor. Investing in financial markets involves risk, and each reader should make their own decisions independently and, if necessary, consult with a licensed professional.

Summary

Common questions on this article's topic

What drives stock market prices, fundamentals or emotions?

What is the Fear and Greed Index?

What are the most common behavioural biases in investing?

What does it mean when stock prices are detached from earnings?

Is buying when there is fear a good investment strategy?

How can I manage my emotional reactions to market fluctuations?

What is behavioural finance?

What is market sentiment?

What are animal spirits in the stock market?

What is market psychology?

What is herd mentality in investing?

If you have any thoughts, questions, or feedback, feel free to drop me a message at mail@richardgolian.com.

LinkedIn

LinkedIn

Related articles

If I take a certain risk, how much can I gain, and how much can I lose?

In April, in the first part of this series, I wrote about an AI prediction system I had started building on my own machine. At the time the software was a few hours old and the prediction record was empty. The record since then has shown one thing: the system does not yet understand the market it is being asked to forecast. It can pull macro context, book value, earnings. But it cannot put those together into something that helps it understand the price.

Prague, 13 May 2026. On my way to work I started thinking about something that stayed with me for days. If most routine work on a computer disappears in the next ten years, and a large share of repetitive manual work disappears with it, what happens to the flow of money? Who pays whom for what? Which economic layers will exist, how large will they be, and what relationships will run between them? This is the six-layer map I sketched as an answer.

More articles

The same task, two models. Fable 5 against Opus 4.8. On paper Fable is the better model, with a larger context and stronger specs. And still it lost. Opus handled the task with a single round of checking for 721,000 tokens, while Fable needed nine rounds and burnt through 2.78 million tokens. The difference was not in the model, but in how I set the task. And I know it, because I measured it.

A few weeks ago I installed a small local AI model on my laptop that watches a live camera feed. I turned the webcam on in the dark, and in near total darkness it recognised me and the objects in the room. That such things exist, I have known for a long time. What opened my eyes was the accessibility. I installed it in one prompt, free, and it runs entirely on my machine, sending data nowhere.

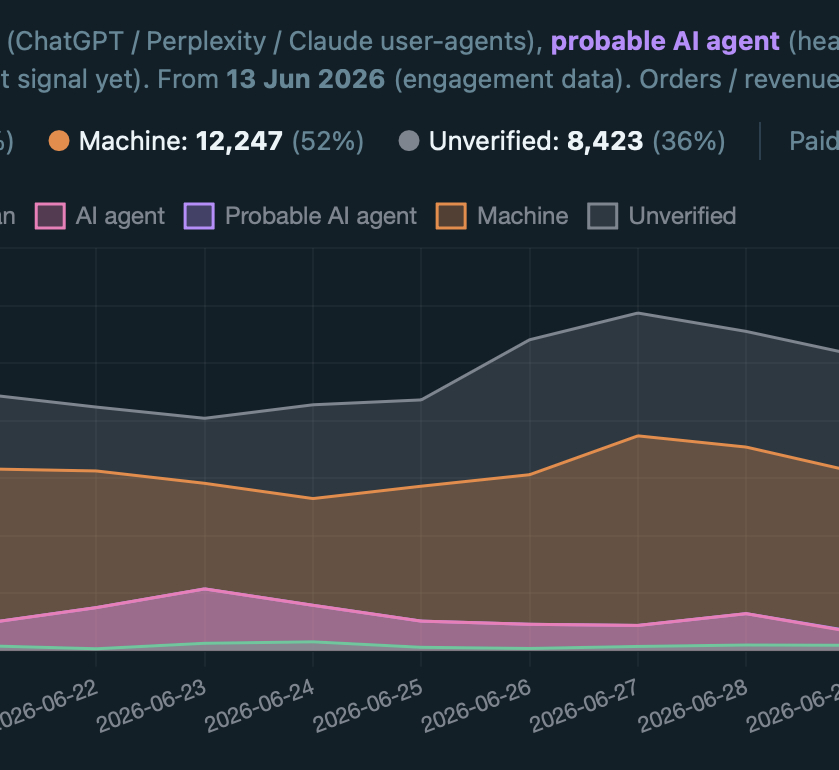

I once wrote about building my own privacy-friendly analytics tool. It had bot detection from the first version, yet it was not enough. Direct visits took a strangely high share of my traffic. When someone claims that 20% of their visits are bots and 80% are humans, I used to think the same. Today I would say the opposite ratio is closer to the truth. This is how I got there.

I have Heidegger and my notebook beside me. I am asking where all of this is heading, where artificial intelligence is taking us.

Seventy per cent. That is where the first AI output begins, even when you give it the full company context and the best examples from the past. We are talking about the kind of output that cannot be defined programmatically. It is more complex. Often it is creative work. On one repeated type of output I reached eighty per cent within a week. Every further percentage point is harder than the one before.

For a long time we treated the internet as the main road. The place where work and relationships happen. Yet most of what we see on it today is, or soon will be, AI-generated: text, images, profiles and comments. The internet is turning into an online game full of bots, where you cannot be sure that a human is on the other side of anything. So I ask: was the online world the main road, or only a temporary detour that part of us will return from, back offline?

A few days ago I interviewed a senior marketer. An experienced man, years of practice. I asked him about AI. He said he barely uses it. He had one bad experience with the output and decided he was too senior for it to add value when it is not perfect. I know the other side too: professionals who automate everything that can be automated.

Europe does not have the capacity to face a full-scale, mass drone war of the kind we see in Ukraine. Three dependencies weaken it: China supplies the physical material for defence systems, the United States supplies capabilities Europe does not have, and twenty-seven states cannot agree how fast, or who pays. Rearmament plans exist, but they are being carried out slowly.

AI produces the graphic, the newsletter and the product page faster than a person. What is left for the one who used to do it is the judgement, knowing whether the output is good. But most people have worse judgement than AI. And whoever cannot judge quality cannot delegate either. How do you tell whether yours is the judgement a company relies on, or the kind it can replace?

Four days in Catalonia. No computer, no AI, almost no social media. I bought this notebook so that I could write down what I would think about, and what I would come across and learn on the trip.