Article

In 2025, the Slovak economy recorded the slowest growth among the V4 countries. How did Slovakia move from the position of the “Tatra Tiger”, one of the fastest-growing economies in the EU, to the bottom of the ranking? And what could change the future of the Slovak economy?

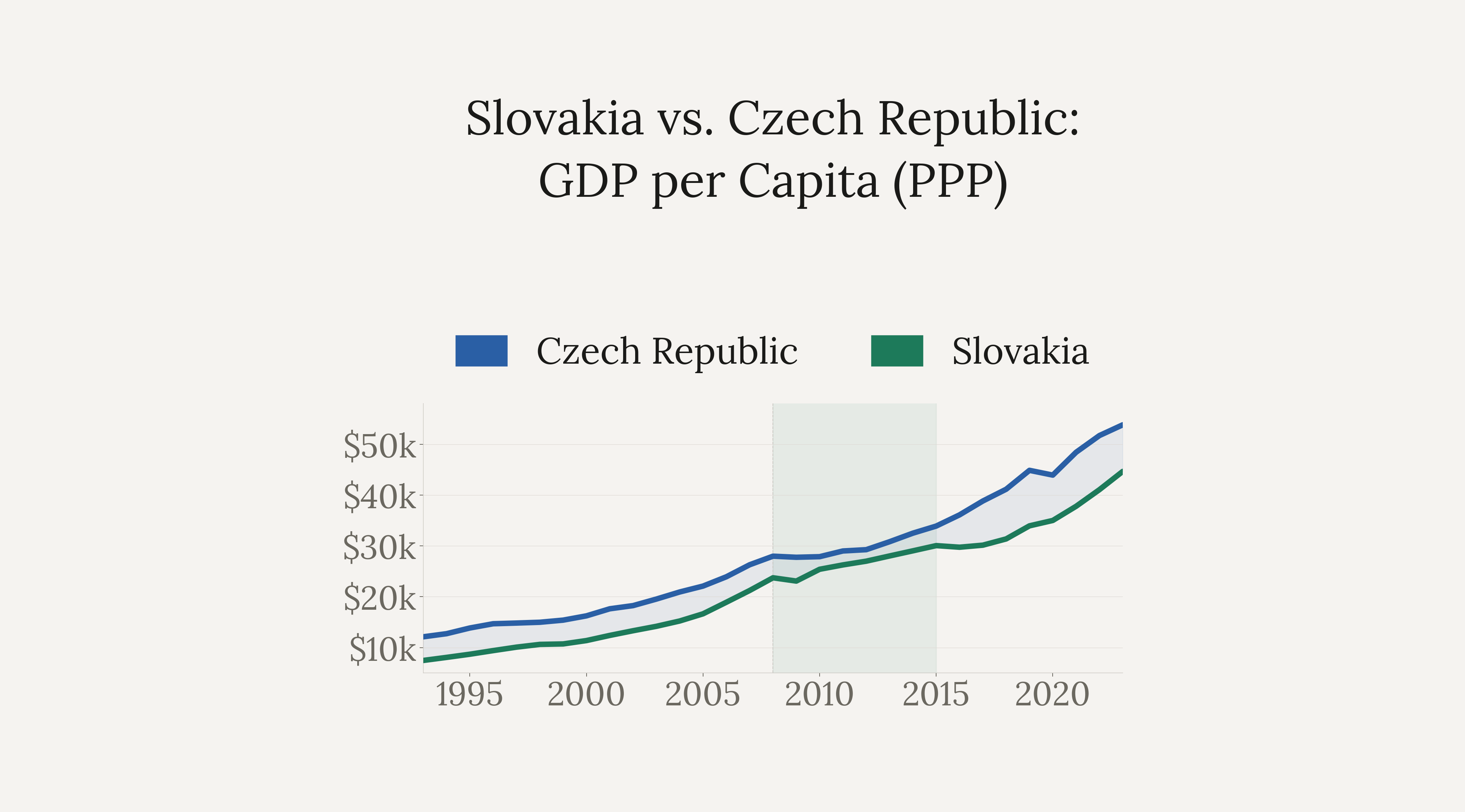

When I arrived at university in Prague in 2016, the latest available data on economic performance, such as GDP per capita in purchasing power parity, showed a clear trend. Slovakia was catching up with Czechia, and it seemed that if the pace continued, it might even overtake it.

It was not just about the data. Czech classmates, especially those studying economics, would bring it up themselves at student events. They said they envied us, mainly for the economic reforms of the early 2000s and the speed at which the Slovak economy was growing.

It felt good.

At the time, I had what now seems like a rather bold expectation: just a few more years and Slovakia would surpass its “older brother” economically and in wages. Of course, we had our problems. But there was also visible progress.

That ended very quickly.

What happened, and how can it be reversed?

The Tatra Tiger (2000–2008): How Slovakia Became One of the Fastest-Growing Economies in the EU

Slovakia went through a period when it was referred to as the “Tatra Tiger.”

Between 2004 and 2007, we were among the fastest-growing economies in the EU, with annual growth of around 6%. In the fourth quarter of 2007, year-on-year growth reached about 14%, among the highest in the OECD, though the figure was inflated by one-off pre-tax stockpiling; underlying growth was closer to 10%.

At the same time, we significantly closed the gap with Czechia. From roughly two-thirds of Czech GDP per capita (PPP) in 1993, we reached around 91% in the period 2010–2013, the closest we have ever been.

This was preceded by concrete steps. The two governments of Mikuláš Dzurinda between 1998 and 2006 launched major reforms: privatisation, opening the economy to foreign capital, and EU accession in 2004. A key step was the 2004 tax reform, a flat 19% rate for personal income, corporate income, and consumption. Slovakia became the first OECD country to implement such a system. This was combined with zero dividend tax and a more flexible labour code.

The cumulative volume of foreign direct investment increased from $2.1 billion at the beginning of 1999 to $18.45 billion by the end of 2006, nearly a ninefold increase in seven years. By the end of 2006, FDI had surged to record levels, though its FDI stock per capita still trailed the Czech Republic and Hungary, the region's leaders.

Slovakia became attractive for capital, and the Slovak economy was widely seen as one of the most promising emerging economies in Central Europe.

Slovakia’s Economic Decline in 2026: Why Growth Has Slowed Down

Today, Slovakia is no longer as attractive to investors.

New companies are not entering Slovakia at the same scale as before, and even domestic ones are leaving. One example is GymBeam, a company with roots in Košice, which moved its holding structure to Austria after a €110 million investment.

Founder Dalibor Cicman described it clearly: Austria offers a more stable and predictable business environment.

The latest ranking of business environment predictability by the World Intellectual Property Organization placed Slovakia 115th out of 139 countries. Within the V4, Slovakia ranks last. Within the EU, it is near the bottom.

GymBeam is not an exception.

In 2025, 7,708 companies were dissolved in Slovakia, the highest number in six years. The economic decline of Slovakia is not just a statistic. It is the daily reality of companies that are leaving or shutting down.

Continue reading for free

Enter your email to keep reading for free. This also subscribes you to my monthly newsletter. No spam, unsubscribe anytime.

Summary

Common questions on this article's topic

What was Slovakia's Tatra Tiger period?

How much foreign investment did Slovakia attract during its reform period?

Why is Slovakia's economy declining?

How close did Slovakia get to catching up with Czechia economically?

What is the V4 and how does Slovakia compare to its neighbours?

Can Slovakia reverse its economic decline?

Is Czechia or Slovakia growing faster?

What is Slovakia's GDP per capita?

Is Slovakia a rich country?

If you have any thoughts, questions, or feedback, feel free to drop me a message at mail@richardgolian.com.

LinkedIn

LinkedIn

Related articles

In every conflict, Slovaks are winners. Why? Because they are always on both sides.

“Unforgivable, unjustified. It can never be forgotten.”

More articles

The same task, two models. Fable 5 against Opus 4.8. On paper Fable is the better model, with a larger context and stronger specs. And still it lost. Opus handled the task with a single round of checking for 721,000 tokens, while Fable needed nine rounds and burnt through 2.78 million tokens. The difference was not in the model, but in how I set the task. And I know it, because I measured it.

A few weeks ago I installed a small local AI model on my laptop that watches a live camera feed. I turned the webcam on in the dark, and in near total darkness it recognised me and the objects in the room. That such things exist, I have known for a long time. What opened my eyes was the accessibility. I installed it in one prompt, free, and it runs entirely on my machine, sending data nowhere.

I have Heidegger and my notebook beside me. I am asking where all of this is heading, where artificial intelligence is taking us.

Seventy per cent. That is where the first AI output begins, even when you give it the full company context and the best examples from the past. We are talking about the kind of output that cannot be defined programmatically. It is more complex. Often it is creative work. On one repeated type of output I reached eighty per cent within a week. Every further percentage point is harder than the one before.

For a long time we treated the internet as the main road. The place where work and relationships happen. Yet most of what we see on it today is, or soon will be, AI-generated: text, images, profiles and comments. The internet is turning into an online game full of bots, where you cannot be sure that a human is on the other side of anything. So I ask: was the online world the main road, or only a temporary detour that part of us will return from, back offline?

A few days ago I interviewed a senior marketer. An experienced man, years of practice. I asked him about AI. He said he barely uses it. He had one bad experience with the output and decided he was too senior for it to add value when it is not perfect. I know the other side too: professionals who automate everything that can be automated.

Europe does not have the capacity to face a full-scale, mass drone war of the kind we see in Ukraine. Three dependencies weaken it: China supplies the physical material for defence systems, the United States supplies capabilities Europe does not have, and twenty-seven states cannot agree how fast, or who pays. Rearmament plans exist, but they are being carried out slowly.

AI produces the graphic, the newsletter and the product page faster than a person. What is left for the one who used to do it is the judgement, knowing whether the output is good. But most people have worse judgement than AI. And whoever cannot judge quality cannot delegate either. How do you tell whether yours is the judgement a company relies on, or the kind it can replace?

In April, in the first part of this series, I wrote about an AI prediction system I had started building on my own machine. At the time the software was a few hours old and the prediction record was empty. The record since then has shown one thing: the system does not yet understand the market it is being asked to forecast. It can pull macro context, book value, earnings. But it cannot put those together into something that helps it understand the price.

Prague, 13 May 2026. On my way to work I started thinking about something that stayed with me for days. If most routine work on a computer disappears in the next ten years, and a large share of repetitive manual work disappears with it, what happens to the flow of money? Who pays whom for what? Which economic layers will exist, how large will they be, and what relationships will run between them? This is the six-layer map I sketched as an answer.

Four days in Catalonia. No computer, no AI, almost no social media. I bought this notebook so that I could write down what I would think about, and what I would come across and learn on the trip.