Article

It is no secret that the stock market is primarily driven by two sentiments: the fear of evil and hope for good. Within these broad emotions, we encounter speculation on rising share prices and the anticipation of future earnings. Conversely, we also find the fear of falling stock prices, economic crises, recessions, and collapses.

I devoted part of my university studies to understanding moods—what they are and how they change. Therefore, it is not surprising that this topic also interests me in the context of the stock market.

How I analyse the stock market

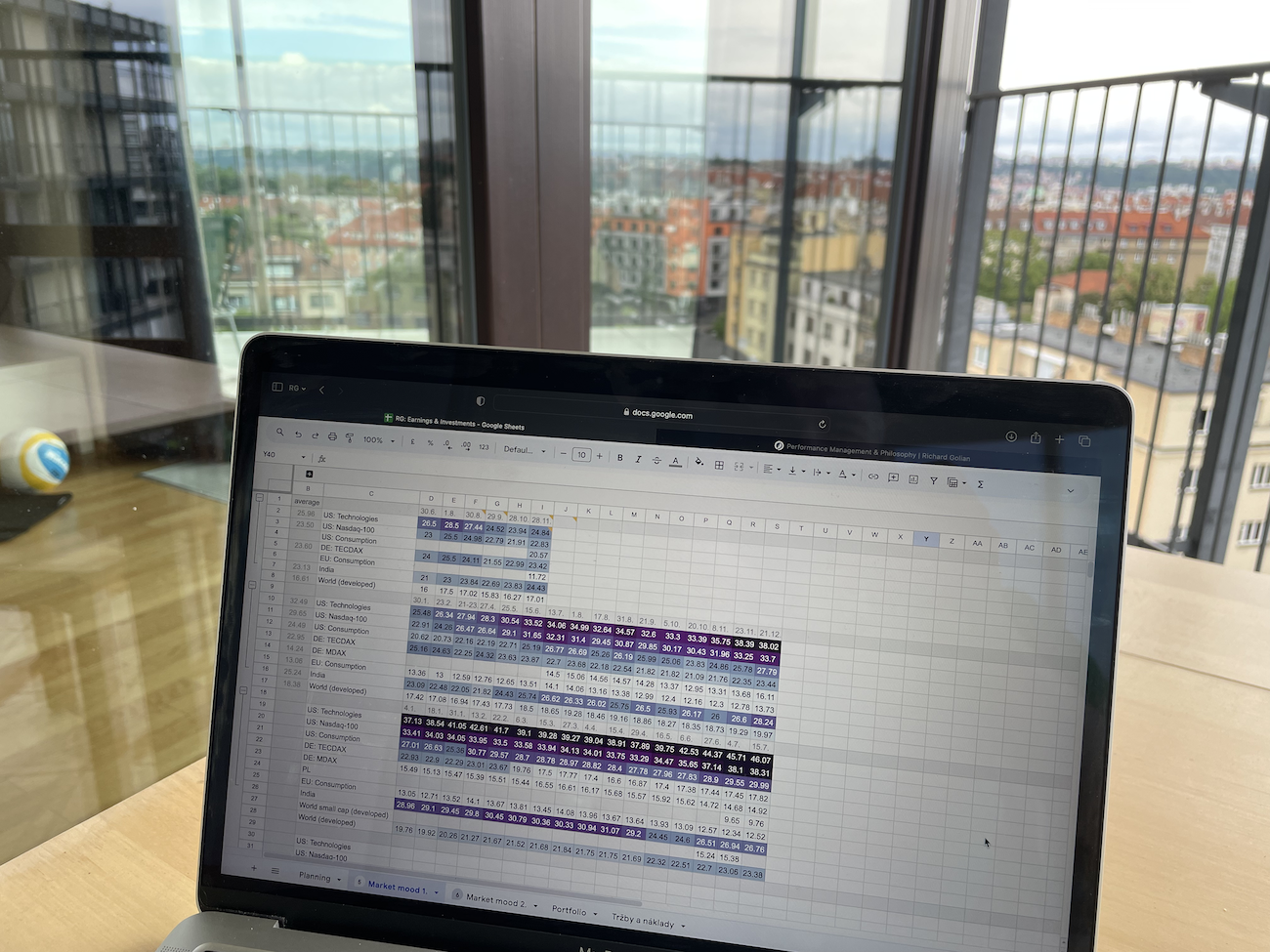

A mood directed towards the future, such as hope for growth or fear of downturns, can be observed through various data. I find it logical to track asset prices within specific segments (geographical or sectoral) in relation to how these segments generate earnings and their value. I compare this data with historical data within the same segment, data from other segments, and the entire stock market's performance.

I use data published by various indexes and ETF funds. As you might gather, I am not analysing individual shares but collections of shares grouped by specific criteria (read more about stock indexes and ETFs). Since 2022, I have been tracking this data, documenting what the media says about the economy and the stock market, and noting factors that could influence sentiments. This forms my “mood thermometer.”

Join the Library

Full access to my thoughts, personal stories, findings, and what I learn from the people I meet.

Join the Library — €29.99 per yearGet the full article by email and feel free to reply if you want to discuss it further.

Disclaimer

This article is intended for informational and educational purposes only. It does not constitute financial advice, a recommendation to buy or sell any securities, or a guarantee of future market performance. The views expressed are solely those of the author, who may also be an investor. Investing in financial markets involves risk, and each reader should make their own decisions independently and, if necessary, consult with a licensed professional.

Summary

Common questions on this article's topic

What drives stock market prices — fundamentals or emotions?

What is the Fear and Greed Index?

What are the most common behavioural biases in investing?

What does it mean when stock prices are detached from earnings?

Is buying when there is fear a good investment strategy?

How can I manage my emotional reactions to market fluctuations?

If you have any thoughts, questions, or feedback, feel free to drop me a message at mail@richardgolian.com.

Related articles

If I take a certain risk, how much can I gain — and how much can I lose?

I am building an AI system to predict the S&P 500. It runs on my own machine, uses free public data — yfinance, FRED, the Shiller dataset — and grades every forecast against reality. This series documents the build itself: the decisions, the methodology, the mistakes. What I will eventually share from the running system is a separate question, and an honest one.

Interesting opportunities often appear where nothing seems to be happening.

More articles

Yesterday I could not tear myself away from the computer. When I lifted my head, it was half past eight in the evening. I had been sitting alone upstairs for about three hours.

Will AI take my job? A certified Google trainer told me in June 2024 that my profession would cease to exist. Twenty-two months later, my job title has not changed — but ninety percent of what I do during the day is different. I have delegated more of my thinking to AI agents than I thought possible. I am not afraid. This is why, and what it means for anyone asking the same question.

One hour. Fifty-five minutes. That is how long it took to build what a Czech software firm had quoted at over €50,000. I built it with Claude Code. Not a prototype. Not a proof of concept. A working tool — the one the company actually needed. By the evening of the same day, it was running on staging. This is not about Claude Code. It is about what Claude Code exposes.

I have conducted roughly one hundred and fifty practical interviews over the past four years. Fifty for data specialist roles. A hundred for advertising and performance marketing specialists. Almost every one of them involved sitting down with a candidate over a practical task — something close to a real problem we actually need to solve at the company. Not theory. Not trivia. Applied problem-solving. Over time, I started noticing a pattern.

Before you can teach AI to understand anything, you need to see what it is hiding from you.

The moment other people needed access to it, the problem changed completely. It was no longer about whether the agent could learn. It was about who gets to teach it.

I wanted to build an agent that doesn't just assist. One that acts.

This is what I learned about local vs cloud AI, and why I switched to Claude Code.

What happened — and how can it be reversed?